Automakers and their suppliers are facing increasingly stringent fuel economy and emissions control requirements. This situation has already occurred before the recent diesel engine emission scandal, but it is now more stringent.

This has led automakers to demand more and more sophisticated reprocessing technologies, and vehicles that have not used post-processing techniques in the past also require post-processing systems. To ensure that this type of aftertreatment system works properly, we clearly need more sophisticated powertrain control. In fact, Mercedes has been installing particulate filters for certain models with gasoline engines since 2014, such as the W222 S500. The company said that it will gradually expand the use of particulate filters as the engine upgrades.

As with post-processing improvements, control strategies are becoming more complex, and more and more vendors are beginning to adopt model-based control rather than relatively simple map control techniques. Transitioning to model-based control usually means higher processing requirements. In some cases, a specific accelerator IP can be used, but a more common approach is to support model-based control directly through the processor core. This requires floating point support; and to ensure efficient execution, it is necessary to introduce some specific mathematical operations to help.

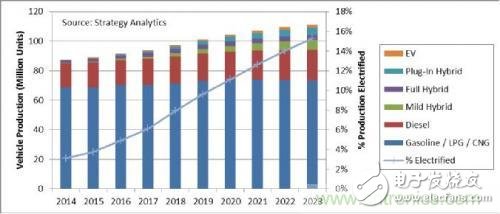

Although the share of electric vehicles in global vehicle production is still relatively small, there is no doubt that this share will surely grow significantly as emission indicators tighten and automakers continue to introduce more cost-effective and outstanding products. .

Research by strategy firm Strategy AnalyTIcs shows that the share of production of various types of electric vehicles in total vehicle production is expected to increase from 5% in 2016 to 15% in 2023.

Light vehicle production by type of power system

The total production of hybrid/electric vehicles is expected to increase from 3.3 million in 2015 to 11.6 million in 2020, with a compound annual growth rate of over 28%. This rate far exceeds the average annual growth rate of 1.6% for traditional power vehicles, and is much higher than the average annual growth rate of 3.3% of total vehicle production. It is estimated that by 2023, the market demand for electric vehicles will further increase to more than 17 million.

There are many different types of electric cars. According to their degree of electrification, they can be roughly divided into:

Mild Hybrid Vehicles – Motor power is typically less than 15 kW and is only used to provide torque assistance without pure electric drive. Among all hybrid vehicle types, this category is ranked second in growth rate, with a compound annual growth rate of 45% from 2015 to 2020. This growth rate is largely dependent on the successful introduction of 48V technology. This 48V mild hybrid car is expected to grow significantly in the European market as major automakers are actively developing cost-effective gasoline engines to replace diesel engines.

Full hybrid vehicles – motors with powers typically above 30 kW can drive the car independently without the assistance of an internal combustion engine. The batteries used in these cars are usually small, so the pure electric cruising range is often only a few kilometers. This category has the slowest growth rate, with a compound annual growth rate of only 8% from 2015 to 2020 – but still well above the overall market growth of 3.3%. This segment is currently the most popular and mature (such as the Toyota Prius), so it is more difficult to continue to grow. In addition, some of the demand will be transferred to plug-in hybrid vehicles.

Plug-in hybrids are similar to full-hybrids and are equipped with powerful motors, but the batteries are much larger and can be charged with an external power source, so the pure electric range is much longer. This type of car offers a "two-for-one" solution: pure electric cruising range to meet daily commuting needs, and long-distance travel with the help of gasoline engine cruising range (and fast refueling). This category will grow at the fastest rate, with a CAGR of 54% from 2015 to 2020. As a result, the production of plug-in hybrid vehicles is expected to surpass full hybrid vehicles by 2020.

Pure electric vehicles are not equipped with petrol or diesel engines. The growth rate in this category can be ranked third, and the compound annual growth from 2015 to 2020 will exceed 34%, although the current base is still very small. To achieve the expected growth rate, major automakers also need to launch new models. In the future, costs and cruising range will continue to be factors that constrain the promotion of such vehicles.

Powertrain processor is a huge market that continues to grow

The changes in the power system layout, combined with the emissions and fuel consumption pressures of traditional power vehicles, have jointly promoted the demand for power system controllers and embedded processors. At the same time, hybrid vehicles powered by internal combustion engines and electric motors need to control these two systems. Complex algorithms are needed to determine the power output ratio of the two power sources to meet the driver's demand for dynamic torque. Battery management systems also require supervision and control of charge/discharge and thermal management of (usually lithium ion) battery packs. In addition, plug-in hybrid and pure electric vehicles also need to be equipped with a car charger controller, so the light power system may require six 32-bit microcontrollers.

Even for a purely electric vehicle that is conceptually simpler, its control strategy can be very complicated: the electric motor usually needs to cope with the torque demand for acceleration and deceleration, because such vehicles usually use regenerative braking technology.

Some models also have multiple motors installed to achieve higher performance levels. The dynamic control elements responsible for torque vector control and front/rear torque distribution also need to be managed and controlled.

In addition to all of these performance requirements, the market is increasingly demanding functional safety. The driver's direct control of the torque output is less and less, so it must be ensured that the motor can be pre-judged and responded safely under all conditions.

In addition, since the release of the ISO 26262 “Road Vehicle Functional Safety†standard in 2011, all automotive applications have become more and more critical to functional safety. Regarding the meaning of functional safety to the power system, the battery management system for electric vehicles and hybrid vehicles can be used as an example. The Tesla electric car uses a large 90kWh lithium battery pack that carries the equivalent of 77kg of TNT explosives. Although this number is less than the energy carried in a conventional power car's fuel tank, proper battery thermal management and charge management (responsible by the electronic control unit) is critical to ensuring safe driving.

Semiconductor manufacturers need support in this area, including specific product design features (such as dual-core lockstep, ECC memory protection and bus) and design flows (such as safety manuals and support for IEC 61508 / SIL 3, ISO 262626 / ASIL D) .

The last challenge that power system control needs to overcome is the centralization of control. The high-end models currently on the market are equipped with more than 100 independent electronic control units. It is common to have separate controllers for basic internal combustion engine control, valve control (eg BMW Valvetronic systems), gearbox control, and traction motor/drive/battery for hybrid vehicles within the powertrain. Many automakers are looking to integrate multiple control functions into a smaller but more powerful electronic control unit, especially in the luxury car market. Such controllers may be multiprocessor devices, each of which may be equipped with multiple cores and run multiple applications. The ability to run multiple operating systems and virtualize tasks through hypervisors will become increasingly important, not only for the infotainment sector, but also for all automotive applications.

At the Ludwigsburg Automobil Elektronik Kongress in June 2016, presentations and discussions from participants showed that BMW, Mercedes and Audi are all pursuing a centralized strategy for future automotive architecture. This task is obviously very difficult, and it is impossible to move directly from high dispersion to high concentration. From this point of view, the so-called "domain controller" architecture type will be more widely adopted. This architecture treats the integration of functions within a single domain (eg, a power system) on a car as a single controller.

Not long ago, BMW made a prediction on the possible outcome of this trend in a statement about the launch of autonomous vehicle platforms. BMW believes that such a car will eventually have only two large controllers: one responsible for controlling the vehicle and the other controlling the infotainment platform. This is a long-term trend that is unlikely to have any impact on the automotive market until 2020. However, the investment cycle of semiconductors is very long, so to meet these new needs, we must act now.

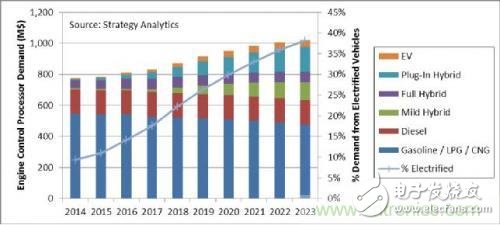

Driven by these ever-changing and demanding requirements, the processor market for engine control applications is expected to exceed $1 billion by 2023. About 9% of this demand comes from the original application for light vehicles.

Engine Control Application Demand for Processors (Million USD)

Among these engine control applications, processor demand from electric vehicle power systems is growing much faster than conventional gasoline and diesel-powered vehicles. As shown above, by 2023, more than 37% of engine control processor demand will come from electric vehicles. This ratio is significantly higher than the 15% share of electric vehicles, because many electric vehicles are hybrid vehicles and require control of gasoline/diesel engines and motors/inverters/batteries.

By 2020, an ordinary pure gasoline-powered car would require a processor worth about $7 to run the engine control application.

In the case of plug-in hybrids, the processor required for engine control is significantly more valuable and will exceed $34 by 2020.

Inspiration

Most of today's powertrain processors use proprietary architectures, but there are already signs that they will change in the future. All semiconductor manufacturers serving the automotive industry face a huge challenge: how to invest huge sums of money to upgrade existing proprietary architectures so that they continue to serve the next generation of power systems. Demand is always changing, and when/whether to upgrade the product line will be the key to decision making. If you have a ready-made solution that includes both the necessary security features and the processes/documents for security-related applications, the time-to-market for new designs will be greatly reduced. In the long run, as car control becomes more centralized, some automakers, including BMW, have begun to study how to centralize all important vehicle dynamics control systems into one module. This process will be complemented by the advent of more automated cars. Powertrain control technology is shifting from a large number of decentralized control boxes to a smaller number of more powerful control devices. In this context, the transition from a separate, proprietary structure to a unified standard architecture seems to be more attractive.

Foldable Laptop Stand,Convenient Foldable Laptop Stand,Foldable Laptop Stand Aluminum,Foldable Ergonomic Adjustable Laptop Stand

Foldable Laptop Stand,Convenient Foldable Laptop Stand,Foldable Laptop Stand Aluminum,Foldable Ergonomic Adjustable Laptop Stand

Shenzhen ChengRong Technology Co.,Ltd. , https://www.chengrongtech.com